SomerCor specializes in helping small business owners looking to buy, expand or refinance a commercial building or equipment through the SBA 504 Loan. The 504 program terms set it apart from any conventional loan on the market. The financing structure supports both startups and businesses in growth mode with strategic capital considerations. A Certified Development Company (CDC), like Somercor, and a traditional lender, partner to help a small business owner obtain the loan.

During these unprecedented times, the need for capital is amplified for many small businesses. However, there is not a one-size-fits-all solution. Here are three reasons the borrower-friendly terms of the SBA 504 loan may be the best fit for some small businesses during the COVID-19 crisis and beyond:

Below-Market Interest Rates Means Lower Monthly Payments:

Right now, interest rates are among the lowest in program history. Rates have been consistently below 4% since August 2019. In July 2020, the interest rate on the 504 loan reached a new record low! Sign up here to receive our monthly email to be the first to know the updated rate.

The resulting blended rate between the lender portion and the SBA’s 504 portion makes the monthly payments for the project more affordable, particularly for small businesses.

Long-Term Fixed Financing Means No Surprise Balloon Payments:

In addition to a lower down payment, borrowers have the option of 10, 20 or 25 year loan terms. Small businesses don’t have to worry about the prime lending rate going up and can calculate the exact amount of their mortgage payments. This eliminates surprise balloon payments and allows for more accurate long-term planning.

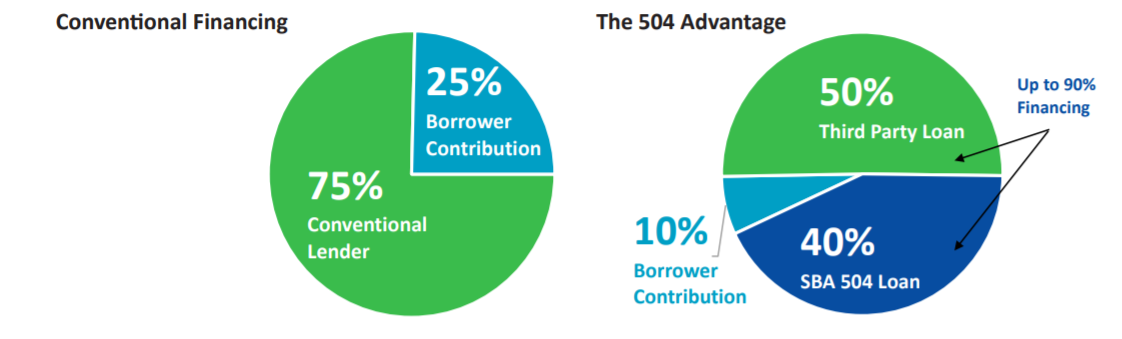

Less Money Down Means Freed Up Working Capital:

The 504 program offers up to 90% financing for established businesses. This means that a borrower only needs to put down 10% of the total project cost. The lender puts forth 50% while the SBA, through a CDC, covers the remaining 40%.

This financing structure frees up working capital that would normally be designated for paying off loans, to instead be reinvested back into growing the business.

Click here for additional details on the financing structure of the 504 loan program and view the chart below for an illustration of how a 504 loan stacks up against conventional financing for a fixed asset.

Margaret Griffin EVP, Chief Lending Officer mgriffin@somercor.com LinkedIn Profile |

Brian Comiskey EVP, Chief Credit Officer bcomiskey@somercor.com LinkedIn Profile |

Elisabeth Williams VP, Loan Officer ewilliams@somercor.com LinkedIn Profile |

Eric Bacon VP, Loan Officer ebacon@somercor.com LinkedIn Profile |